Use CSRD as a driver for your sustainability strategy

While fewer organisations may fall within its remit, the European Union’s Corporate Sustainability Reporting Directive (CSRD) provides a useful framework to help define your strategy. The process can guide you to develop smarter long-term approaches which future-proof your business, improve stakeholder relationships and strengthen your reputation.

Why is it important to have a robust ESG strategy?

Climate change, legislation, competitive pressures and more are placing industrial companies across Europe in a sustainable transition. Specific risks and uncertainties include:

- Rising claims of greenwashing

- Geopolitical unrest and high energy prices

- Shortage of raw materials, water, etc

- EU legislation including CSRD, Clean Industry Deal, Corporate Sustainability Due Diligence Directive (CSDDD)

- Investor demand for transparency and accountability

- Supply chain disruption due to climate change

- Increasing societal pressure

The benefits and opportunities of a robust sustainability strategy include:

- Future-proof your business and increase resilience

- Comply with new EU legislation

- Attract and retain talent

- Gain a competitive edge

- Improve access to capital

- Reduce costs and enhance efficiency

- Strengthen stakeholder trust

- Integrate various transitions into one holistic sustainability transition

Book your free 30 minutes consultancy now

Choose Haskoning as your ESG strategy partner. With all the expertise needed for defining your strategy and reporting under one roof, we are here to help with accurate, timely preparation of your company’s sustainability reporting.

How can CSRD still contribute to a robust sustainability strategy?

The Corporate Sustainability Reporting Directive (CSRD) can still play a crucial role in helping you develop a sustainability strategy bringing long-term benefits to your business:

- Strategic transition to a future-proof business: The CSRD requires companies to create strategic transition plans. By identifying and addressing sustainability impacts, risks and opportunities, sustainability is embedded into the core of your business strategy. It results in a more resilient and future-proof organisation.

- Engagement and communication increase trust: There is a need to report in detail on sustainability activities, risks and opportunities. Communicating more effectively with stakeholders - customers, investors and regulators - builds trust and eases access to capital.

- Common standards highlight competitive advantage: Uniform reporting requirements within the CSRD ensure all companies adhere to the same sustainability standards. It fosters fair competition and prevents greenwashing, making it easier to demonstrate sustainable competitive advantage.

- Wide-ranging input can strengthen your supply chain: CSRD reporting extends to direct and indirect business relationships across the value chain. This gives opportunities to cooperate more closely with your value chain partners, strengthening the resilience of your supply chain.

- Broad scope leads to smarter long-term strategies: The double materiality principle helps you to identify and prioritise sustainability matters from both impact and financial perspectives and improves strategic decision making.

How can we help? Empowering transformation towards sustainable industry

Find your way through the ever-growing complexity of sustainability reporting, stakeholder communication and performance management with a trusted, independent partner. We help you identify your impacts, choose those which are most material, and define your strategic goals. Our support extends to strategy drafting and implementation.

Partner with us to turn your sustainability challenges into opportunities for growth, ensuring your sustainability goals are actionable and impactful.

Benefit from our substantive knowledge of ESG themes to guarantee a holistic approach. Our strong track record combines technical knowledge and practical implementation to deliver measurable impact for your organisation through feasible, integrated strategic plans. We can help you with:

- Value chain mapping: Gain insights into risks, opportunities and efficiencies across your operations.

- Materiality assessments: Prioritise the most critical issues for your business and stakeholders.

- Strategic ESG alignment: Develop comprehensive strategies that meet compliance requirements, enhance resilience and drive long-term value.

- Data driven solutions: Integrate data management and digital solutions in the decision-making process for better informed decisions and strategies.

Experts in ESG management and strategy

Substantive knowledge on ESG topics

Multi-disciplinary experience in developing corporate statements and reporting

A holistic approach to your sustainability strategy

Your implementation experts

What is the Corporate Sustainability Reporting Directive (CSRD)?

The Corporate Sustainability Reporting Directive is a European Union (EU) directive which changes the way organisations must disclose and report information on environmental, social, and corporate governance (ESG) performance. It is aimed at improving transparency and comparability of sustainability reports among EU organisations and their value chain. This enables stakeholders to make informed decisions and drive sustainable investments towards organisations that prioritise ESG performance.

Organisations need to report on risks and opportunities arising from social and environmental issues, and on the impact of their activities on people and planet. It includes environmental issues such as climate change risks, pollution and biodiversity, social impacts like human rights, as well as governance factors like employee matters, anti-corruption, and anti-bribery matters.

The CSRD reporting is a mandatory framework for companies which meet the threshold and is more extensive and highly specific in its disclosure requirements covering ESG compliance. CSRD also holds a voluntary standard (VSME) for companies outside the scope of the CSRD.

We have been supporting businesses with non-financial corporate reporting and ESG strategies since their inception. This includes frameworks such as International Sustainability Standards Board (ISSB), Task Force on Climate-Related Financial Disclosures (TCFD), Global Reporting Initiative (GRI), Sustainability Accounting Standards Board (SASB). Together, we can help you overcome implementation and preparation challenges to report accurately against your CSRD standards and timelines.

Meet your CSRD timelines

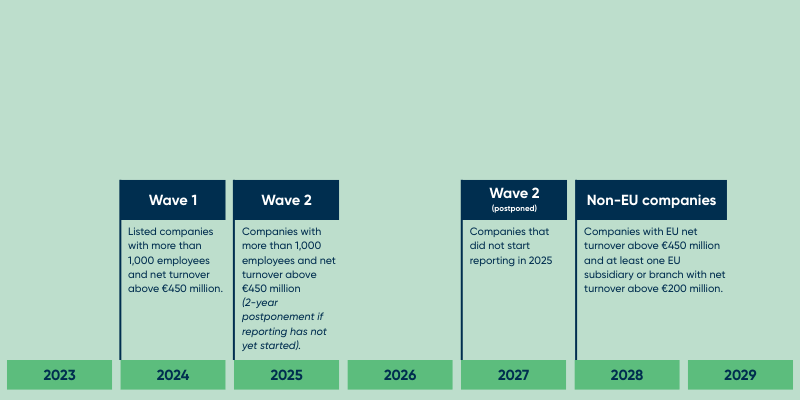

The Omnibus packages, as discussed in the EU in 2025, have changed the reporting obligations for many organisations. Under the adjusted plans, around 10.000 organisations in Europe will still be subject to the CSRD (previously around 50.000), but more organisations will need to supply information on their environmental and social impact to clients and suppliers.

Current criteria - CSRD affects organisations that meet the following criteria:

- Net turnover above €450 million per annum;

- More than 1,000 employees (annual average).

Current timelines:

- 1 January 2025 for organisations already subject to the Non-Financial Reporting Directive (NFRD), for the 2024 financial year (Wave 1).

- 1 January 2026 for organisations not subject to the NFRD, for the 2025 financial year (Wave 2), provided they meet the thresholds. Companies that did not start reporting in 2025 (prior to the Omnibus package) will have a later start date, with first reporting for the 2027 financial year.

- Non-European organisations that meet the thresholds will be required to report in 2029, based on 2028 data.

Simplified reporting requirements (expected to come into force mid 2026):

European Sustainability Reporting Standards (ESRS) are being revised and simplified (with fewer qualitative datapoints and most reporting on quantitative datapoints). Sector-specific standards to be dropped. Reasonable assurance standard to be removed (limited assurance only). Voluntary reporting based on a standard for SMEs (VSME) and reporting standards for non-EU companies (NESRS) are being developed by the European Financial Reporting Advisory Group (EFRAG).

Possible changes to CSRD by ESG Omnibus I and II packages

Changes to CSRD are in prospect following the European Commission’s presentation of the Omnibus package in early 2025. It adjusts timelines, thresholds for companies subject to reporting, and simplifies reporting guidelines (ESRS). This package potentially reduces the number of companies in the CSRD’s scope by about 80%.

Note however that the Omnibus is not yet approved and effective – planned changes and timing are outlined below:

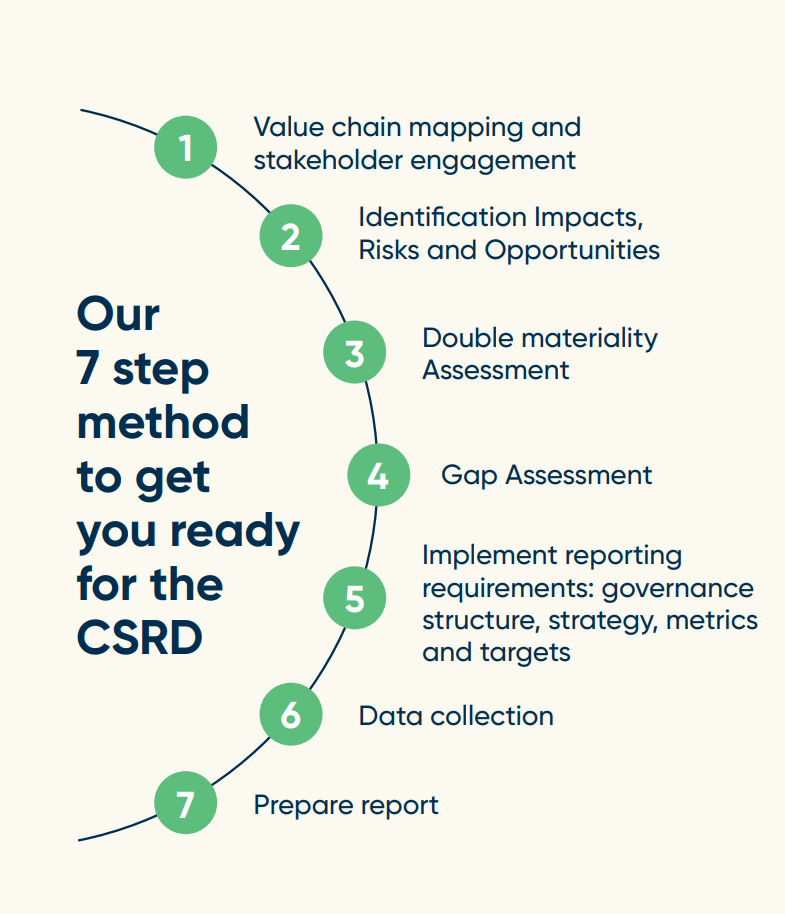

Our 7-step method

Download our simple, structured 7-step approach which, together with our strategic ESG management services, ensure qualitative and fully compliant non-financial reporting.