Report: Canada trade diversification and port capacity outlook

JolkeHelbing

SavvasKonstantinidis

Canada’s trade diversification strategy has regained focus since the Trump administration introduced import tariffs. A successful diversion of the current Canadian trade with the US towards overseas trade partners will imply an increase in cargo routed via Canadian ports.

Haskoning analysis, led by a team of maritime business consultants, presents alternative markets for Canadian importers and exporters – as well as the impact of diversification on port throughputs.

Analysis headlines:

- If Canadian exporters and importers look for alternative markets, Haskoning analysis shows that Northern Europe, the Far East, and the Mediterranean emerge as the most promising.

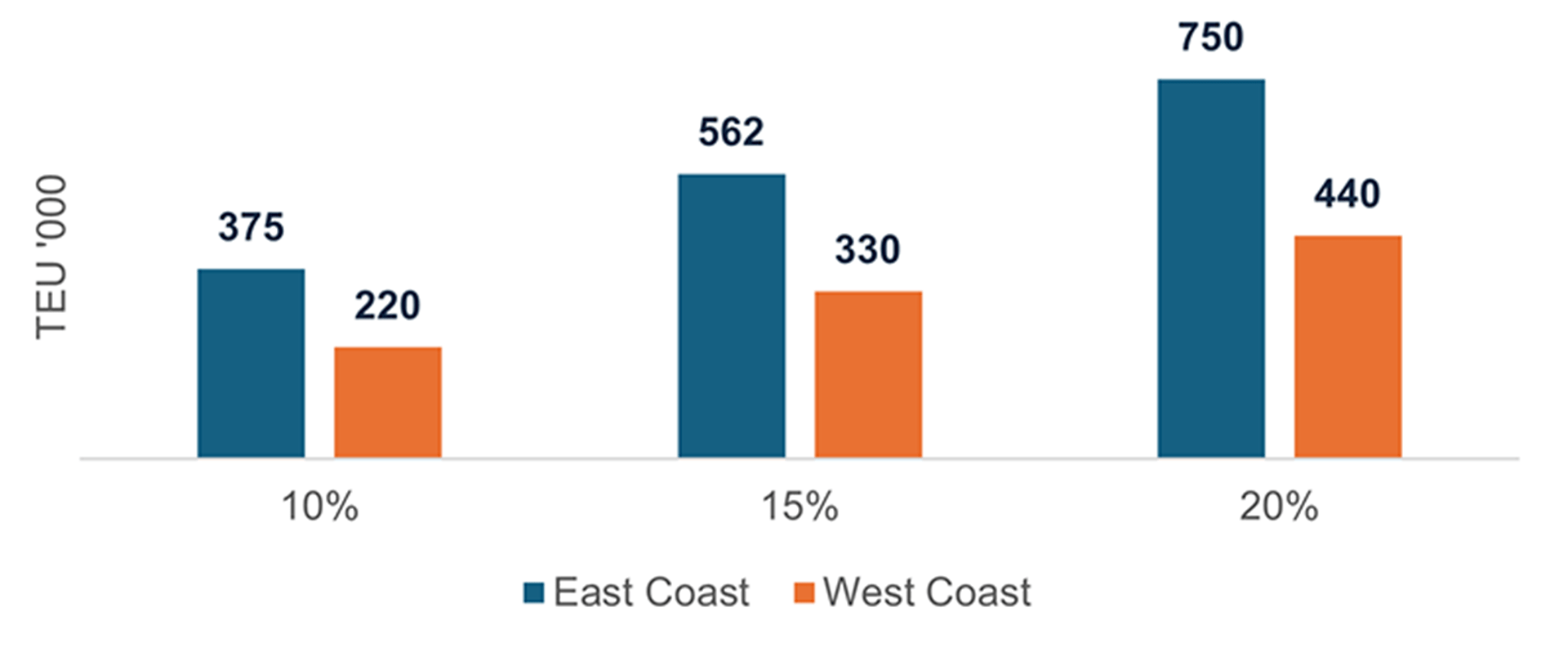

- In all trade diversification scenarios analysed (10%, 15% and 20% of estimated containerized US-Canada trading volumes), East Coast ports are expected to handle the majority of the additional throughput.

- This increased throughput could reach nearly 750,000 TEUs per year for the East Coast in a 20% scenario. Representing a 35% increase in port volumes relative to its current throughput.

- West coast ports are projected to handle around 440,000 TEUs per year in a 20% scenario – a 10% increase on current throughput.

- Even Prime Minister Mark Carney’s fast-tracking of major port terminal infrastructure projects in Vancouver (West) and Montreal (East) may not be enough to meet the possible container demands in successful diversification scenarios.

US-Canada trade relations today

In 2024, Canada and the US traded approximately 455 million tonnes of goods, with around 50 million tonnes1 identified as potential containerised cargo. Based on historical tonne-to-TEU ratios at Canadian ports, 50 million tonnes equate to roughly 5 million TEUs.

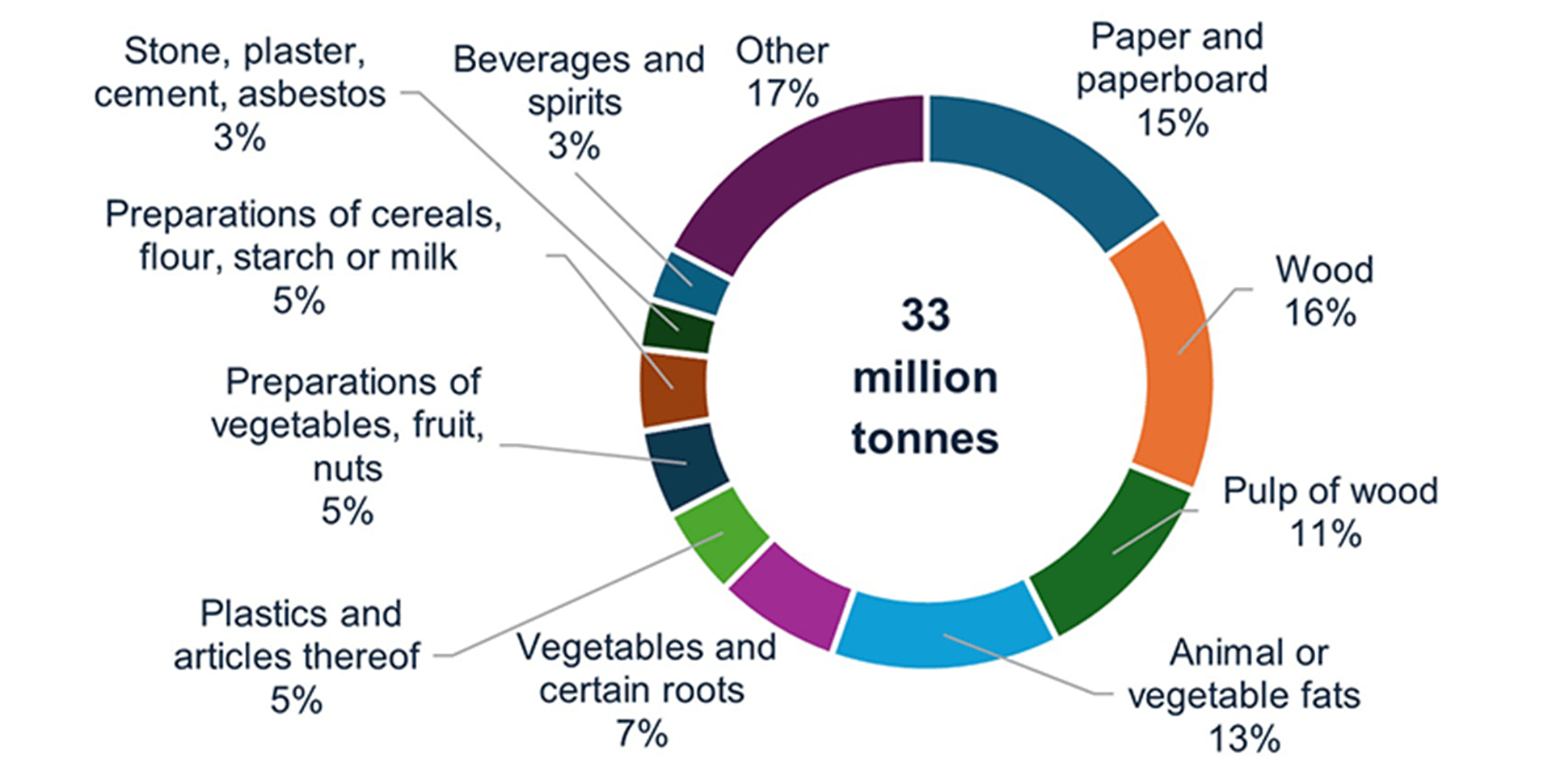

Figure 1 shows the ten key potential containerised commodities exported to the US, representing more than 80% of the total. Key export commodities are wood products, paper, and vegetable oils.

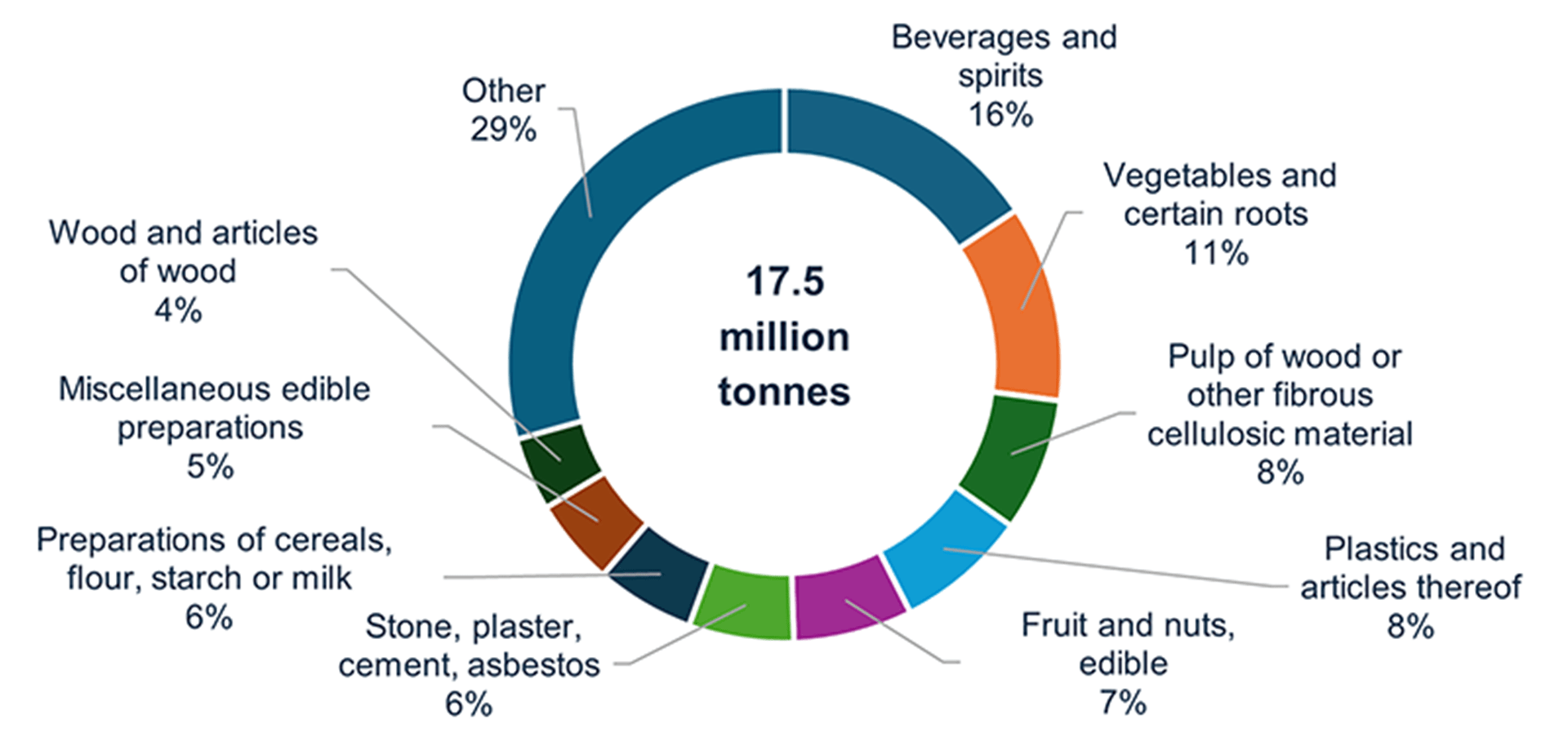

Estimated containerised Canadian imports from the US are dominated by paper products, beverages and vegetables, as shown in Figure 2.

Unpicking the knot: Scenario analysis of alternative markets

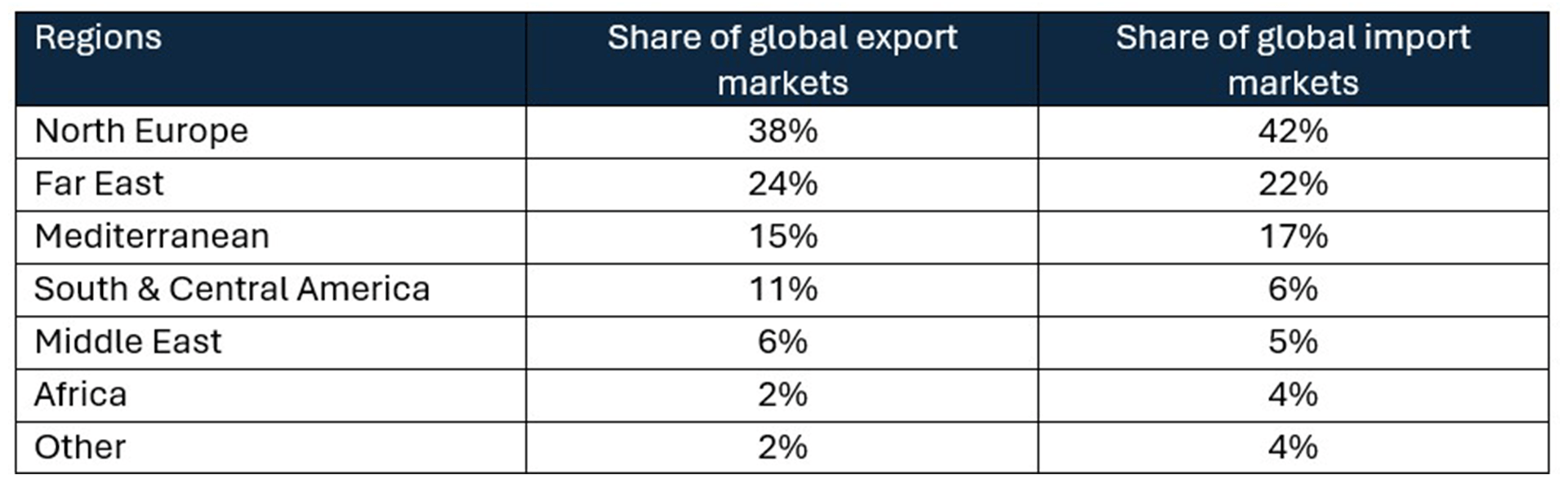

To assess the potential impact of trade diversification, containerised volumes are mapped to either Canada’s West or East coast ports based on likely destination or origin markets.If Canadian exporters and importers look for alternative markets, our analysis shows that Northern Europe, the Far East, and the Mediterranean emerge as the most promising alternative markets (Table 1)2.

This analysis implies that Canadian exporters and importers will more often use Canada’s East coast ports in case of a trade diversification. For example, wood products are more likely to be exported via East coast ports due to strong demand in the UK, Germany, and France.

Based on our findings, East coast ports are expected to handle 63% of redirected imports and 67% of redirected exports, driven by strong demand in high-income regions like North Europe and the Mediterranean. The West coast, oriented towards Asian markets, accounts for 32% of exports and 36% of imports. A small share remains unassigned, due to niche markets or flexible routing.

Pushing ports to the limit: The implications of trade diversification

Figure 3 illustrates the coastal distribution of diverted containerised volumes under three diversification scenarios (10%, 15%, and 20%). Haskoning added a fixed share of empty containers on top of the potentially additional throughput3.In all cases, East coast ports are expected to handle the majority of the additional throughput, reaching nearly 750,000 TEUs per year in the 20% scenario. West coast ports are projected to handle around 440.000 TEUs per year in that scenario.

This represents a 35% increase in East coast ports volumes relative to its current throughput, driven by increased trade with Northern Europe and the Mediterranean. For the West coast ports this represents a modest 10% increase, mainly linked to Asian markets.

A long-term question with no easy answers

Although the success of Canada’s trade diversification strategy is still uncertain, its potential impact on Canadian ports is substantial. Meanwhile, according to Scotiabank, Canada’s current federal spending estimates forecast that road and rail will account for 80% of infrastructure CAPEX in the coming fifty years. While intermodal capacity is crucial in building robust and holistic supply chains, the lack of port infrastructure investment will raise flags as possible trade diversification increases.Even with planned major port infrastructure projects being fast-tracked more recently through the will of a newly elected government – including Vancouver Fraser Port Authority’s c.$3 billion mega-terminal on the West Coast, and Montreal Port Authority’s c$1.6 million Contrecoeur terminal project on the East – the new capacity may be quickly outstripped by demand in case of success trade diversification away from the US.

These findings show that a successful Canadian trade diversification has the potential to stretch port capacity earlier than expected and port capacity is needed sooner rather than later.

Read more about maritime challenges and our solutions

Maritime

Maritime